Our goal is to give you the tools and confidence you need to improve your finances. Although we receive compensation from our partner lenders, whom we will always identify, all opinions are our own. Credible Operations, Inc. NMLS # 1681276, is referred to here as "Credible."

If you’re planning to attend a graduate program, a Graduate PLUS Loan could help you cover the cost.

Grad PLUS Loans are specifically designed for graduate as well as professional students and could cover up to your school’s cost of attendance (minus any other financial aid you’ve received).

Here’s what you should know about Grad PLUS Loans:

- What are Grad PLUS loans?

- Grad PLUS loans vs. unsubsidized federal loans vs. private student loans

- Requirements for Grad PLUS loans

- How to take out a Grad PLUS Loan

- Using private student loans as a Grad PLUS loan alternative

What are Grad PLUS loans?

Graduate PLUS Loans are a type of Direct PLUS Loan available to graduate and professional students. These loans typically have higher interest rates compared to other types of federal loans, such as Direct Subsidized and Unsubsidized Loans.

They also come with a loan disbursement fee that’s deducted from the amount borrowed.

To apply for Grad PLUS Loans, you must complete the Free Application for Federal Student Aid (FAFSA), as well as a separate Direct PLUS Loan Application. You’ll also have to undergo a credit check.

However, interest will continue to accrue on the loan while you’re in school and during the six-month grace period. You can choose to pay the accrued interest or allow it to capitalize, meaning it will be added to the loan principal.

Learn More: How to Get a Student Loan for Online College

What is a Direct PLUS Loan?

Graduate students can take advantage of the benefits of federal student loans with a Direct PLUS Loan. These loans help graduate and professional students pay for higher education classes. Students who want to receive a Direct PLUS Loan should complete the FAFSA. Direct PLUS Loans currently have a fixed interest rate of 8.05%.

You can take out up to the cost of attendance with a Direct PLUS Loan, minus any other financial assistance you receive, such as scholarships and grants.

If you take out Direct PLUS Loans for graduate or professional school, you don’t need to make loan payments while attending school. You may make interest-only payments while in school or allow the interest rate to capitalize and be added to the loan balance.

Grad PLUS Loan limits

Unlike other types of federal student loans, Grad PLUS Loans don’t have a specific limit on how much you can borrow per year, nor do they have an aggregate limit.

Instead, you might be able to borrow up to your school’s certified cost of attendance, minus other financial aid you’ve received.

If you decide to take out a private student loan, be sure to consider as many lenders as possible to find the right private student loan for you. Credible makes this easy — you can compare your prequalified rates from our partner lenders in two minutes.

Check Out: Average Cost of College in the U.S.

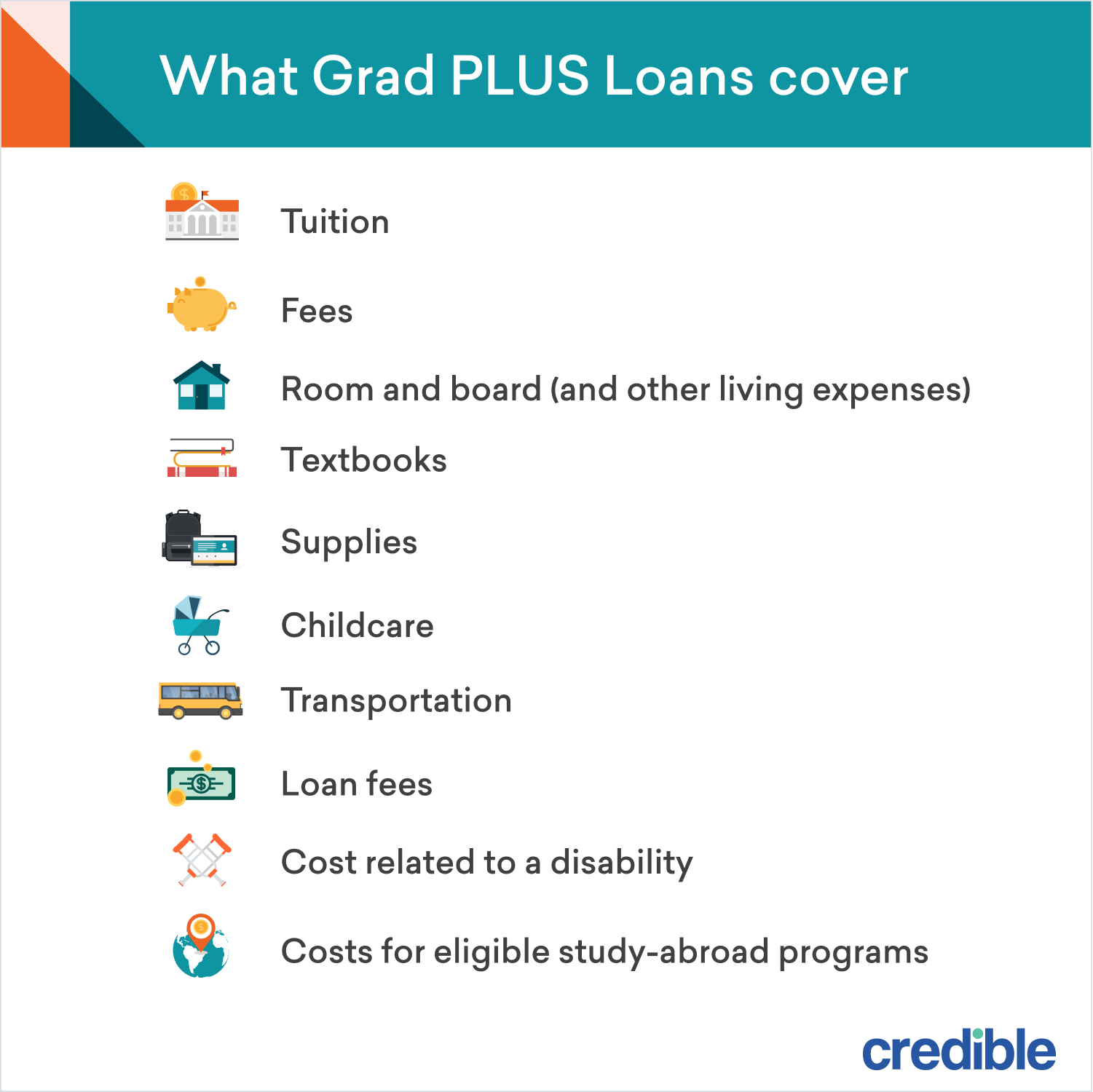

What Grad PLUS Loans cover

In addition to covering the cost of tuition and school supplies (like books, pens, and notebooks), you can use Direct PLUS Loan funds to cover other living expenses, like housing, transportation, and even child care. Additionally, you can use the funds to pay for costs associated with a disability, like computer programs, tape recorders, laptops, and assistive listening devices.

You can also use loan funds to pay for meal plans, food, bus passes, parking passes, and study abroad fees. All living expenses, including medical necessities, toiletries, utilities, and household expenses, are eligible costs.

But you can’t use student loan funds to purchase a vehicle (even if used to commute to school), pay off other debt, or pay for business expenses.

Check Out: Best Private Student Loans

Grad PLUS loans vs. unsubsidized federal loans vs. private student loans

If you’re pursuing a graduate or professional degree, you have two federal loan options: Direct Unsubsidized Loans and Grad Plus Loans.

You could also consider paying for grad school with private student loans, which are issued by private lenders, such as online lenders, traditional banks, and credit unions. Keep in mind that you’ll typically need good to excellent credit (or a cosigner with good credit) to qualify for a private loan.

After you’ve exhausted your federal loan options, private student loans could help fill any financial gaps. Depending on your credit, you might qualify for a better interest rate on a private loan compared to a PLUS Loan.

However, keep in mind that private loans aren’t eligible for the federal benefits and protections that come with Grad PLUS Loans, such as access to income-driven repayment plans and student loan forgiveness programs.

Here are a few key points to keep in mind if you’re considering federal vs. private student loans for grad school:

| Grad PLUS Loans | Direct Unsubsidized Loans | Private student loans | |

|---|---|---|---|

| Interest rate type | Fixed | Fixed | Fixed or variable |

| Interest rate | 8.05% | 7.05% | Fixed rates from (APR):

3.39%+

Variable rates from (APR): 4.13%+ (with Credible partner lenders) |

| Disbursement fee | 4.228% | 1.057% | Typically none |

| Borrowing limit | Up to school’s cost of attendance (minus any other financial aid received) | $20,500 per year ($73,000 aggregate limit) | Up to school's cost of attendance (depending on the lender) |

| Credit check required | Yes (must not have adverse credit to qualify) | No | Yes (must have good to excellent credit or a cosigner to qualify) |

| Interest accrues while in school | Yes | Yes | Yes |

| Payment starts | 6 months after graduation | 6 months after graduation | Depends on the lender |

| Loan term | 10 years (on standard repayment plan) | 10 years (on standard repayment plan) | 5 to 20 years (depending on the lender) |

No matter which type of student loan you choose, it’s important to consider how much that loan will cost you. This way, you can be prepared for any added expenses.

You can find out how much you’ll owe over the life of your federal or private student loans using our student loan calculator below.

Enter your loan information to calculate how much you could pay

With a $ loan, you will pay $ monthly and a total of $ in interest over the life of your loan. You will pay a total of $ over the life of the loan, assuming you're making full payments while in school.

Need a student loan?

Compare rates without affecting your credit score. 100% free!

Checking rates won’t affect your credit score.

Learn More: What to Do if Your Parent Plus Loan is Denied

Requirements for Grad PLUS loans

To qualify for a Grad PLUS Loan, you must meet certain eligibility requirements, including:

- Complete the FAFSA

- Be a U.S. citizen or an eligible noncitizen, such as a permanent resident alien

- Be a graduate or professional student enrolled at least half-time at an eligible school

- Be enrolled in a program leading to a degree or certificate

- Not have an adverse credit history

You don’t need to demonstrate financial need to be eligible for a Grad PLUS Loan, but lenders will check to make sure you don’t have an adverse credit history. If you have things like bankruptcy, late payments, or defaulted loans on your credit report, you may not qualify for a Grad PLUS Loan. But adding an endorser to your application (similar to a cosigner) could help you get approved. You could also consider asking a parent to apply for a Parent PLUS Loan to help cover your education costs.

Graduate students may also apply for a Direct Unsubsidized Student Loan. The Direct Unsubsidized Loan is a federal student loan. Borrowers do not need to show financial need (income level), and they aren’t required to undergo a credit check. Unsubsidized loans will accrue interest while you’re attending classes. Graduate students can borrow up to $20,500 per year.

Learn More: How to Get a Student Loan With No Credit Check

How to take out a Grad PLUS Loan

If you’re ready to take out a Grad PLUS Loan, follow these steps:

- Fill out the FAFSA. Your first step in paying for grad school should be completing the FAFSA. Your school will use your FAFSA results to determine what federal financial aid and federal loans you qualify for.

- Apply for scholarships and grants. Unlike student loans, college scholarships and grants don’t have to be repaid — which makes them a great way to pay for school. There’s no limit to how many scholarships and grants you can get, so it’s a good idea to apply for as many as possible. You might also be eligible for school-based scholarships depending on your FAFSA results.

- Take out federal student loans. After you fill out the FAFSA, your school will send you a financial aid award letter detailing the federal aid you’re eligible for. You can then decide which federal aid and federal loans you want to accept — such as Direct Unsubsidized Loans. If you’d also like to apply for a Grad PLUS Loan, you’ll need to complete a Direct PLUS Loan Application.

- Use private student loans to fill the gaps. After you’ve exhausted your scholarship, grant, and federal loan options, private student loans can help fill any financial gaps left over. While private loans don’t offer federal protections, they do offer some benefits of their own — for example, you can apply at any time and might be able to borrow more than you’d get with a federal loan.

Check Out: How to Get Student Loans for Nursing School

Using private student loans as a Grad PLUS Loan alternative

In some cases, taking out private graduate student loans could be a better choice than Grad PLUS Loans. Here are a few situations where this might make sense:

- You have good to excellent credit. If you have good credit, meaning a credit score of 700 or higher, you might qualify for a lower interest rate on a private student loan compared to a PLUS Loan. Having a lower rate could help you save money on interest charges over the life of your loan. You’ll also be able to choose between a fixed or variable rate.

- You want a longer repayment term. The standard loan term on Grad PLUS Loans is 10 years — though you could potentially extend your repayment term by signing up for another repayment plan or by consolidating to a Direct Consolidation Loan. However, if you’d like to start with a longer term right off the bat, you might be able to get a term up to 20 years through a private lender. This could be helpful for longer or more expensive programs, such as law school or medical school.

- You don’t want to pay disbursement fees. Grad PLUS Loans charge some hefty disbursement fees. Private student loans, on the other hand, generally don’t come with disbursement fees, which could save you money. Keep in mind that some lenders might charge other fees — though if you take out a private student loan through one of Credible’s partner lenders, you won’t have to worry about application fees or origination fees.

If you decide to get a private student loan to pay for college, remember to consider as many lenders as you can to find the right loan for you. Credible makes this easy — you can compare your prequalified rates from our partner lenders in the table below in two minutes.

| Lender | Fixed rates from (APR) | Variable rates from (APR) | Loan amounts | Loan terms (years) | Cosigners allowed |

|---|---|---|---|---|---|

Credible Rating

| 3.39%+10 | 5.01%+10 | $2,001* to $400,000 | 5, 7, 10, 12, 15, 20 (depending on loan type) | Yes |

|

|||||

Credible Rating

| 3.99%+1 | 4.97%+ | $1,000 to $350,000 (depending on degree) | 5, 10, 15 | Yes |

|

|||||

Credible Rating

|

3.47%+2,3

| 4.44%+2,3 | $1,000 up to 100% of the school-certified cost of attendance | 5, 8, 10, 15, 20 | Yes |

|

|||||

Credible Rating

| 4.24%+ | 4.44%+ | $1,000 to $99,999 annually ($180,000 aggregate limit) | 7, 10, 15 | Yes |

|

|||||

Credible Rating

| 4.62%+8 | 7.15%+8 | $1,001 up to 100% of school certified cost of attendance | 5, 10, 15 | Yes |

|

|||||

Credible Rating

| 5.75%+ | N/A | $1,500 or $2,000 up to school’s certified cost of attendance (depending on school type and minus other aid received) | 10, 15 | Yes |

|

|||||

Credible Rating

| 3.490%9 - 15.49%9 | 4.54%9 - 14.710%9 | $1,000 up to 100% of school-certified cost of attendance | 10 to 20 | Yes |

|

|||||

your credit score. 100% free! Compare Now |

|||||

Lowest APRs reflect autopay, loyalty, and interest-only repayment discounts where available | Read our full methodology | 10Ascent Disclosures | 1Citizens Disclosures | 2,3College Ave Disclosures | 11Custom Choice Disclosures | 7EDvestinU Disclosures | 8INvestEd Disclosures | 9Sallie Mae Disclosures |

|||||

Keep Reading: 3 Best MBA Student Loans for Business School

Angela Brown contributed to the reporting for this article.