Our goal is to give you the tools and confidence you need to improve your finances. Although we receive compensation from our partner lenders, whom we will always identify, all opinions are our own. Credible Operations, Inc. NMLS # 1681276, is referred to here as "Credible."

More than 43 million adults in the U.S. have student loan debt, according to EducationData.org — so if you get married, there’s a good chance that both you and your spouse will have student loan debt. Considering that the typical graduate has eight to 12 different loans, a married couple could have up to 24 loans to manage — which might make the idea of consolidating student loans with your spouse appealing.

If you consolidate your debt, you’ll end up with just one loan to manage and one monthly payment to remember. As of 2021, PenFed Credit Union is the only lender that allows couples to consolidate their loans together. But you do have other options.

Here’s what you should know about consolidating student loans with your spouse:

- Can you consolidate your loans with your spouse?

- Spousal loan consolidation vs. cosigning your partner’s loan

- Refinancing with cosigner release

- How to refinance a student loan

Can you consolidate your loans with your spouse?

Yes, if you refinance through a lender like PenFed, you can consolidate your student loans with your spouse’s loans. Your spouse could also consider refinancing their student loans with you as a cosigner (or vice versa).

Here’s how these strategies work:

- Spousal loan consolidation: With PenFed, you can consolidate both your and your spouse’s student loans into one new refinanced loan with a single payment.

- Cosigning your partner’s loans: Another option is for your spouse to apply for refinancing with you as a cosigner. While your loans won’t be consolidated together if you’re approved, you’ll share responsibility for the loan with your spouse.

The only option for combining federal loans with your spouse’s loans is through private student loan consolidation, which is very different from federal consolidation. If you refinance federal student loans or consolidate them with a spouse’s debt, you’ll be replacing your federal student loans with a private student loan. This means you’ll lose access to federal student loan repayment options and protections, such as income-driven repayment plans and student loan forgiveness programs.

Learn more: Student Loan Consolidation vs. Student Loan Refinancing

Spousal loan consolidation vs. cosigning your partner’s loans

Here are a few critical differences to keep in mind before deciding whether to consolidate or cosign student loans with your spouse:

Check Out: Federal Student Loan Repayment Calculator — Strengths and Limitations

Spousal loan consolidation

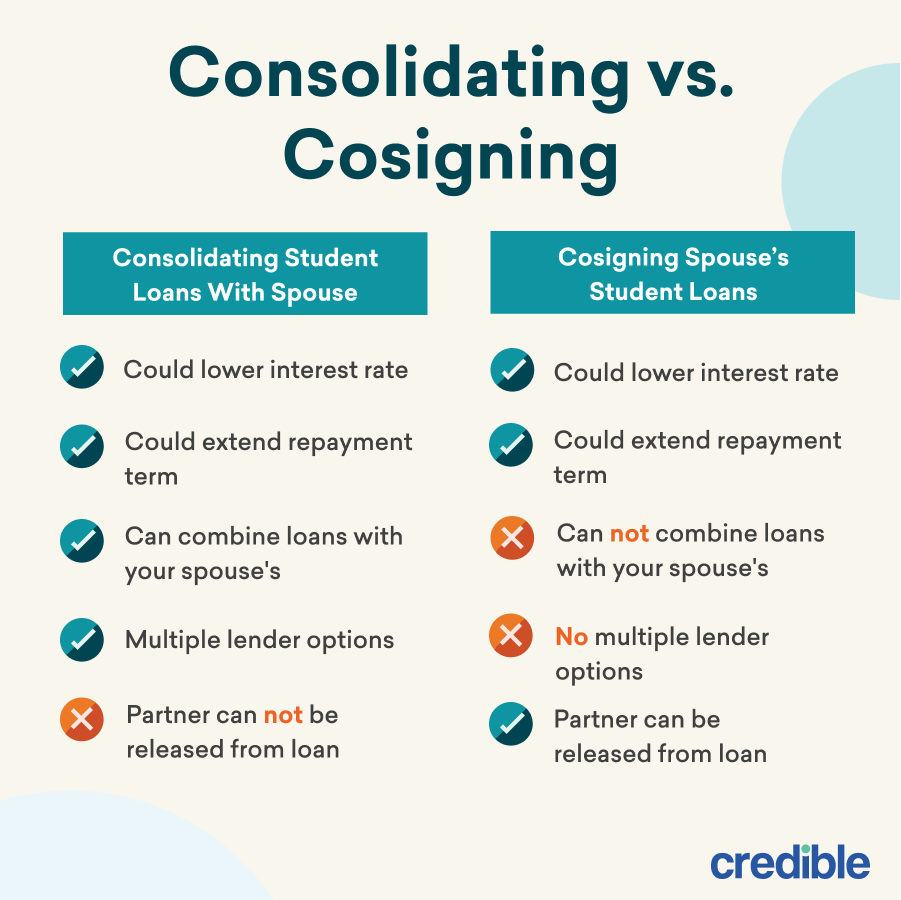

With spousal loan consolidation, the lender will consider your combined income and debt and will determine your interest rate based on the highest credit score and level of education between both of you. This could make it a good option if you are a stay-at-home spouse, earn significantly less than your partner, or didn’t finish college.

Pros

- Could simplify your repayment: Keeping track of multiple student loans with different due dates and amounts can be difficult. If you consolidate your student loans, you and your spouse will have just one loan and payment to manage.

- Might get a lower interest rate: Depending on your and your spouse’s credit, you might be able to lower your student loan interest rate through consolidation. This could save you money on interest and even potentially help you pay off your loan faster.

- Good option for stay-at-home parents: Unlike if you cosigned a loan, your interest rate on a spousal consolidation loan will be determined based on the highest credit score and level of education between you and your partner. This could help you get a lower interest rate than if you refinanced your loan.

Cons

- Difficult to get out of spousal consolidation: Your spouse will be a joint borrower on the loan application and can’t be removed, even if your relationship sours down the line and you separate or divorce. If you split up, you’ll still share equal responsibility for repaying the loans, even if your spouse’s original debt makes up the bulk of the balance.

- Lack of lender options: PenFed is the only lender that allows spouses to consolidate their loans, which means you can’t shop around for a lower rate.

Learn More: Pros and Cons of Consolidating Student Loans

Cosigning your partner’s loans

If you opt to cosign your partner’s loans through refinancing, you’ll have many more lenders to choose from. Additionally, some lenders offer a cosigner release option — this means you could be removed from the loan after a specific number of consecutive, on-time payments are made.

Pros

- Might get a lower interest rate: Depending on your partner’s credit, they might get approved for a lower interest rate through refinancing than what they’re currently paying. Additionally, even if your partner doesn’t need a cosigner to qualify for refinancing, having you as a cosigner could help them get a lower interest rate than they’d get on their own.

- Multiple lender options: There’s a wide variety of student loan refinance companies to choose from. This means that you and your spouse can shop around to find the most favorable rate and terms for your needs.

- Possible cosigner release: Some lenders offer cosigner release after making consecutive, on-time payments for a specific period of time. This means your spouse could remove you from the loan later on, eliminating your repayment responsibility.

Cons

- Will still have multiple loans: While you can refinance and combine your own loans, you can’t combine them with your spouse’s. This means you’ll still have more than one loan to track and repay.

- Might be harder to qualify for: Unlike with spousal consolidation, refinancing lenders typically consider the income, debt, and credit score of both the primary borrower and the cosigner. This could make it harder to qualify compared to spousal consolidation if you or your spouse has poor credit or a low income.

If you decide to refinance your student loans, be sure to consider as many lenders as possible to find the right loan for you and your spouse. Credible makes this easy — you can compare your prequalified rates from multiple lenders in two minutes.

Check Out: When Student Loan Refi Is a Good Idea and When to Reconsider

Refinancing with cosigner release

Several lenders provide the option to have a cosigner released from the loan. This could be helpful if:

- You’re looking to raise your debt-to-income (DTI) ratio, as being released from the loan will lower your debt obligations.

- You or your spouse ever decide to end your relationship, as you’ll have the option of being removed from your obligation.

To qualify for cosigner release, the primary borrower will generally need to make consecutive, on-time payments for a certain period of time — usually one to four years, depending on the lender. They’ll also need to meet the underwriting criteria on their own.

Learn More: Refinance Student Loans With a Cosigner in 3 Steps

Lenders that offer cosigner release

If you want to refinance your student loans with a lender that provides a cosigner release option, remember to consider as many lenders as you can first. This way, you can find a loan that works best for you and your spouse.

Here are Credible’s partner lenders that offer cosigner release:

| Fixed rates from (APR) | Variable rates from (APR) | Min. credit score | Cosigner release offered | |

|---|---|---|---|---|

Credible Rating

| 5.65%+1 | 5.69%+1 | Does not disclose | After 36 months |

Credible Rating

| 6.99%+2 | 6.99%+2 | Does not disclose | After 24-36 months |

Credible Rating

| 4.15%+5 | 5.22%+5 | 700 | After 36 months |

Credible Rating

| 5.31%+4 | 6.83%+4 | 670 | After 48 months |

Credible Rating

| 6.94%+ 7 | N/A | 670 | After 24 months |

Credible Rating

| 4.39%+ | 4.17%+ | 700 | After 12 months |

| Compare personalized rates from multiple lenders without affecting your credit score. 100% free! |

||||

All APRs reflect autopay and loyalty discounts where available | 1Citizens Disclosures | 2College Ave Disclosures | 5EDvestinU Disclosures | 3 ELFI Disclosures | 4INvestEd Disclosures | 7ISL Education Lending Disclosures | 8Nelnet Bank Disclosures |

||||

Check Out: How Often Can You Refinance Student Loans?

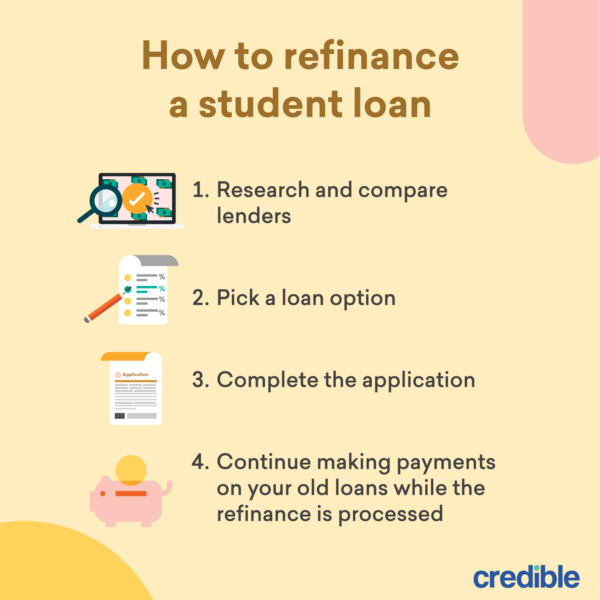

How to refinance a student loan

If you decide to refinance your student loans, follow these four steps:

Check Out: 6 Ways Student Loans Can Impact Your Credit Score

How much can you save by refinancing?

How much you can save through student loan refinancing will mainly depend on the interest rate you qualify for as well as the repayment term you choose. In general, you’ll need good to excellent credit to qualify for the lowest interest rates — a good credit score is usually considered to be 700 or higher.

You could also keep your overall interest costs lower by choosing a shorter repayment term. Plus, several lenders offer lower rates to borrowers who opt for shorter terms.

If you’re wondering how much you could save by refinancing your student loans, use our calculator below:

Step 1. Enter your loan balance

Step 2. Enter current loan information

Step 3. Enter your new loan information to start calculating your savings

If you refinance your student loan at % interest rate, you can save will pay an additional $ monthly and pay off your loan by . The total cost of the new loan will be $.

Does refinancing make sense for you?

Compare offers from top refinancing lenders to determine your actual savings.

Check Personalized Rates

Checking rates won't affect your credit score

1$16,943 savings disclaimer: Savings estimates assume the analyzed consumers will make full, on-time monthly payments for the full life of the loan according to the terms of their promissory notes. Actual savings may be higher or lower. Average $16,943 savings calculation based on (1) information the users shared with Credible about their original loans (such as loan balance, repayment term, and rate) and created an account between Nov.1, 2019 and Dec. 1, 2020; and (2) actual loan terms for those same users who refinanced into a student loan with a shorter repayment term than the weighted average of their previous loan’s(‘) remaining months to full amortization, calculated using information the users shared with Credible . This calculation excludes borrowers who refinanced to a loan of a similar or longer duration or who reported loan terms that deviate from normal user experiences, including: (i) any loan term with less than one (1) year or more than twenty-five (25) years remaining before refinancing; (ii) monthly loan payments greater than $5,000 per month before refinancing; and (iii) any existing loan amount (before refinancing) that deviates more than five (5) percent from the loan amount disbursed upon refinancing. Our calculations do not take into account variable factors such as the borrower’s potential eligibility for loan forgiveness, variable interest rates, deferments, late payments, underpayments, missed payments, or pre-payments. Please note that your actual savings may vary depending on interest rate, balance, loan terms, credit score, and other factors.