Our goal is to give you the tools and confidence you need to improve your finances. Although we receive compensation from our partner lenders, whom we will always identify, all opinions are our own. Credible Operations, Inc. NMLS # 1681276, is referred to here as "Credible."

Mortgage amortization refers to the way your mortgage lender applies your loan payments to your principal balance and the interest due on your loan. In the early years of the loan, most of your payment goes toward interest. As years pass, more of your payment gets applied to the principal balance.

This repayment schedule, or amortization schedule, ensures that your home loan will be paid in full when you make your last scheduled payment. Plus, you start building equity with your very first payment.

Here’s what you should know about mortgage amortization:

- Mortgage amortization is how home loans are paid off

- How mortgage amortization works

- How to make your own amortization table

- How to make your own amortization schedule

Mortgage amortization is how home loans are paid off

The typical home loan has a 30-year term, which equals 360 monthly payments. And when the mortgage loan has a fixed interest rate, your principal and interest payment stays the same for the life of the loan.

An amortizing adjustable-rate mortgage works a little differently. Because the interest rate changes periodically, so do the principal and interest payments.

- A principal payment toward the balance on your loan

- An interest payment on the balance still owed

See how much you’ll owe over the life of your home loan using our monthly mortgage payment calculator below.

Enter your loan information to calculate how much you could pay

With a $ home loan, you will pay $ monthly and a total of $ in interest over the life of your loan. You will pay a total of $ over the life of the mortgage.

Early on, you pay more toward interest than toward the principal balance because more interest accrues each month on the larger principal balance. But each payment chips away at the principal balance, reducing the amount of interest that accrues before your next payment is due.

As the interest diminishes, more of your payment goes to paying down the principal balance. When you make your final payment, you will have repaid the entire amount you borrowed plus all of the interest due on the loan.

Revolving debt like a credit card is non-amortizing. As each payment date arrives, you can make a payment consisting of mostly or all interest and carry the principal balance forward to the next month.

Learn More: How Much a $150,000 Mortgage Will Cost You

Here’s how mortgage amortization works

The first step in working out an amortization schedule is to calculate your monthly payment. Lenders use three variables in that calculation:

- Loan amount: The difference between the purchase price and the down payment

- Interest rate: The annual interest rate for the loan

- Number of payments: The total number of payments you’ll make

From there, lenders use a formula to create the amortization table.

Keep Reading: 30 Mortgage Terms to Know: Ultimate Glossary for Homebuyers

Sample mortgage amortization table

The sample mortgage amortization schedule below bases the calculation on a 30-year, $180,000 loan with an annual mortgage rate of 4.50%. The calculator came up with the payment and the payment breakdown rounded to the nearest dollar.

Though a real mortgage amortization table would show all 360 payments, this hypothetical example shows three months’ worth of payments:

| Payment date | Total payment | Amount applied to principal | Amount applied to interest | Principal balance |

|---|---|---|---|---|

| June | $912 | $237 | $675 | $179,763 |

| July | $912 | $238 | $674 | $179,525 |

| August | $912 | $239 | $673 | $179,286 |

How to make your own amortization table

Creating a table for your mortgage amortization allows a deeper dive into how mortgage loans work and how different scenarios affect your loan.

A full amortization table for a 30 year loan will have 360 entries, and it’s best to use a spreadsheet program to organize the information. There are many options available, and most come with a built in formula for calculating the periodic payment on a loan. Some spreadsheet programs call this the “PMT” function, which automatically calculates your loan payment based on the variables listed previously.

In the screenshots below, we used Google Sheets to build an amortization schedule, but you can use any common spreadsheet program to perform similar functions. (Credible does not endorse Google Sheets or any other spreadsheet program.)

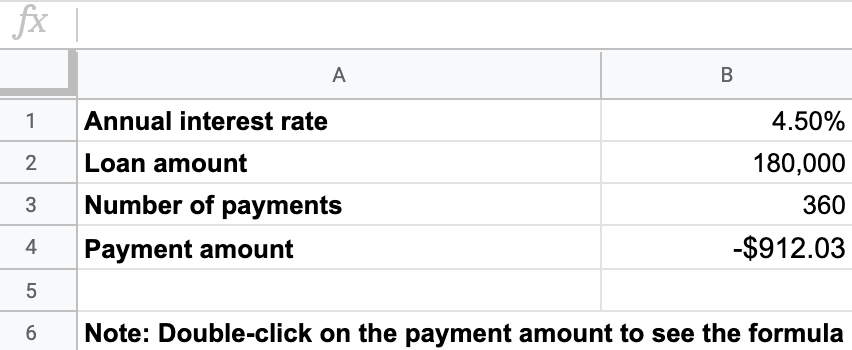

Once you’ve created a new spreadsheet, enter the information needed to calculate your payments.

In the sample spreadsheet below, the exact PMT formula to include is: =PMT(B1/12, B3, B2)

Follow this example, but with your own figures:

Hit the Enter key after filling in B4 to run the PMT formula and display the payment amount. In this case, it’s $912.03. Now, you can use that payment amount to create your amortization schedule in a new spreadsheet.

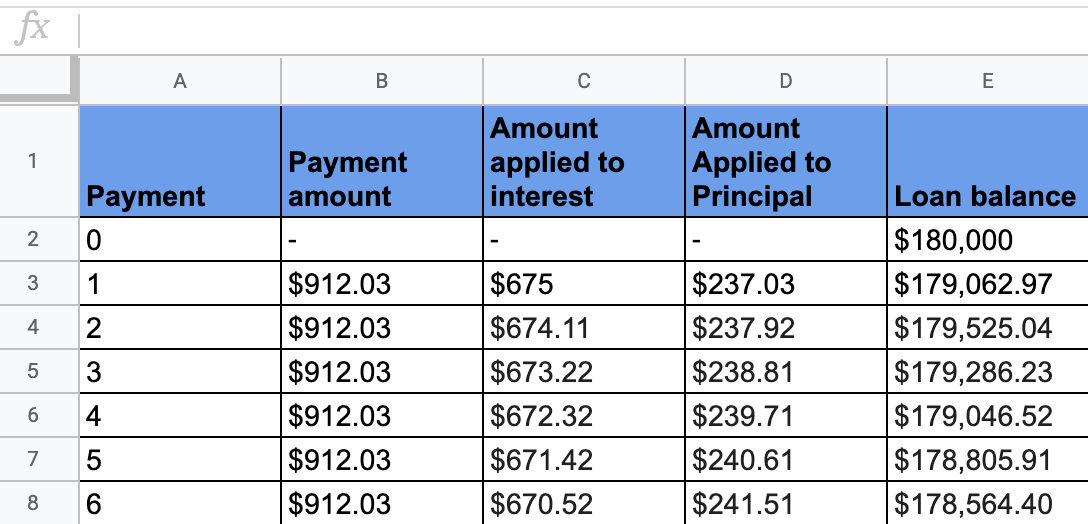

How to make your own amortization schedule

The amortization schedule that follows shows payments one through six, with no rounding. For these calculations only, the loan balance is expressed in mils — one mil equals $1,000.

Here are the step-by-step calculations for dividing Payment 1 between interest and principal:

- $180,000/$1,000 = 180 mil beginning loan balance

- 4.50/12 = 0.375 monthly interest rate

- 0.375 * 180 mils = $675 interest payment

- 912.03 – 675 = $237.03 principal payment

- $180,000 – $237.03 = $179,762.97 balance

Payment 0 indicates the month after you purchase your home and take out your mortgage. You pay mortgage loans after the billing period rather than before — so you don’t make a payment the first month after you close.

Once you’ve figured out the first payment, you can apply the same calculations to each subsequent month using the new loan balance left over after your prior payment until you’ve worked out the schedule for the entire loan.

Once you have this information, you can:

- Set a budget for buying a home

- Test how different down-payment amounts affect your payment and the long-term cost of your loan

- See how much you can save by shopping for the best mortgage rate

- Explore how extra payments, which your lender may apply to pay down your principal, save you money on interest and help you repay your loan faster