The cost of a $600,000 mortgage payment not only depends on the interest rate you receive and the term you choose, but also property taxes and home insurance. If you take out a $600,000 home loan with a 30-year repayment term, your monthly principal and interest could range from $3,597 to $4,195, based on your interest rate.

This guide will inform you about the factors you need to consider when purchasing a home, as well as the possible monthly costs you can expect with a $600,000 mortgage.

Monthly payments for a $600,000 mortgage

The monthly payment for a $600,000 mortgage includes principal and interest, as well as other essential items.

Here’s an overview of a typical mortgage payment:

- Loan principal: The amount your lender loans to you after your down payment. After closing, the loan principal is the remaining amount you have left to pay.

- Interest rate: The fee your lender charges you in exchange for loaning you money.

- Property taxes: The taxes you’ll pay to your local government for your home, which are based on your property’s assessed value. As a homeowner, part of your monthly mortgage payment will go into an escrow account to cover what you owe.

- Homeowners insurance: This protects you if damage occurs to your property. Home insurance also typically includes liability protection if someone gets hurt on your property. As with property taxes, you make a partial payment each month toward your annual premium. That money is set aside by your lender into an escrow account, and is paid to the provider on your behalf.

Note:

Depending on which loan you choose, you may have other costs to consider, too. For example, if you use an FHA loan, you’ll have to pay a mortgage insurance premium (MIP), which will increase your monthly payment.

The table below illustrates what the monthly principal and interest payment would be for a $600,000 mortgage, depending on which interest rate you receive.

Where to get a $600,000 mortgage

Many traditional banks, credit unions and online lenders provide loans for $600,000 or more, but the trick is finding the one with the best offer for you.

Expert tip:

“Shop for a lender early. Try getting pre-approved with several lenders, as each lender can give you a slightly different offer. Compare APRs, closing costs, down payment requirements, and what discounts they offer.” — Valerie Morris, Editor, Mortgages

Once you’ve found the best lender, it’s time to officially submit a loan application. To do this, you may need to provide additional documentation to your lender.

What to consider before applying for a $600,000 mortgage

In addition to your monthly mortgage payment, you should also plan to pay for a down payment, closing costs, upkeep costs and, if applicable, homeowners association dues.

The amount needed for a down payment on a $600,000 house depends on the type of mortgage you choose and what your lender approves you for. Some lenders might require you to pay for mortgage insurance if you make a down payment that’s less than 20%.

Note:

For a $600,000 mortgage, a 20% down payment would cost $120,000.

Also consider ongoing upkeep costs when determining how much house you can afford. A good rule of thumb is to set aside a minimum of 1% of your home’s value. For a home assessed at $600,000, this means you should set aside at least $6,000 a year for future upkeep expenses, such as a new roof or kitchen appliances.

Saving up for a house can take time, so make sure you consider every variable.

Amortization table on a $600,000 mortgage

The amortization schedule largely depends on the loan term you choose. Here’s a breakdown of a $600,000 loan repayment schedule with a 30-year term and a 6% fixed rate.

Here’s the amortization schedule for a $600,000 loan with a 6% fixed interest rate and a 15-year term instead of a 30-year term:

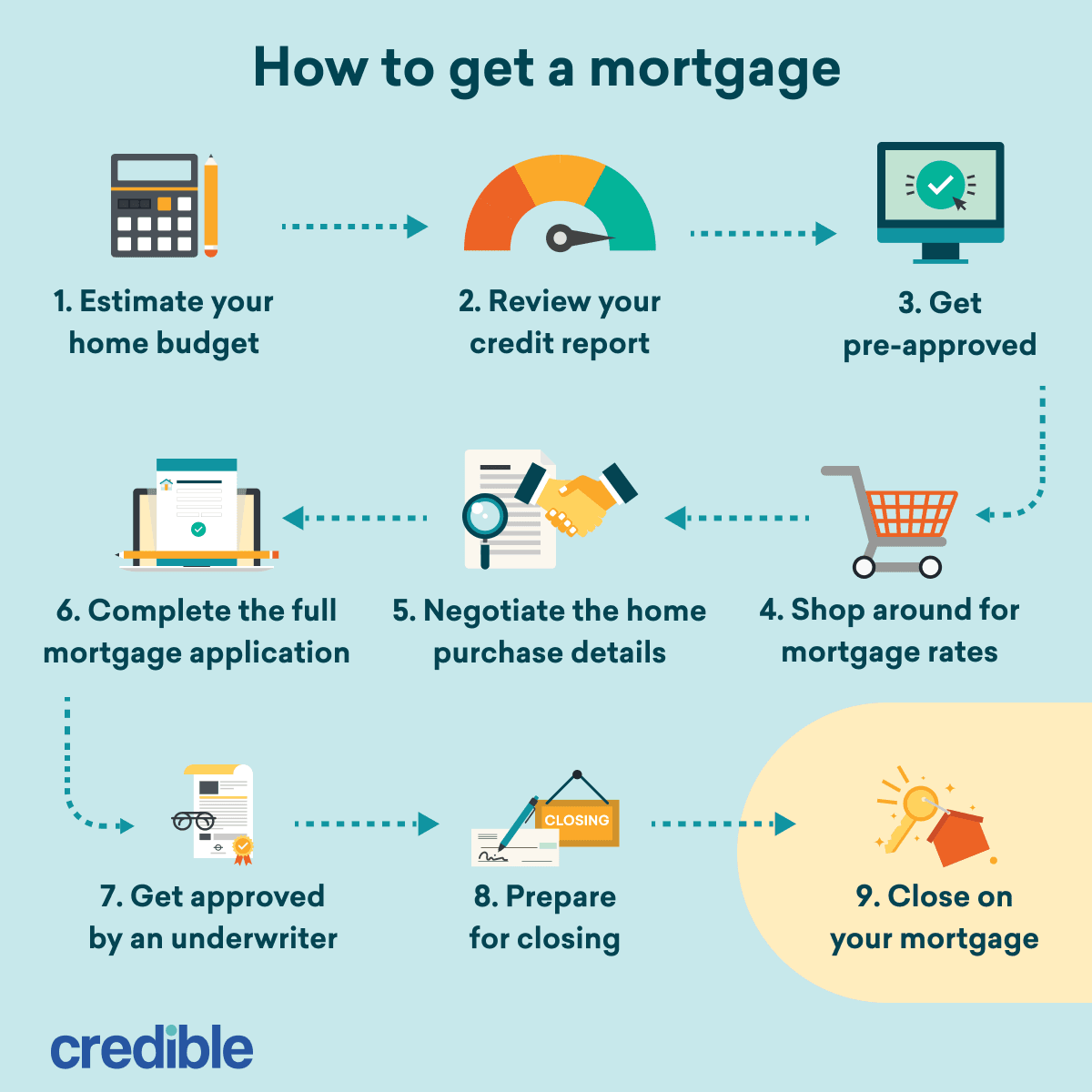

How to get a $600,000 mortgage

When you apply for a mortgage, be prepared to provide significant documentation, including your homebuying budget, income, savings and assets, and credit history.

Here are the steps you’ll take to get a $600,000 home loan:

- Determine what you can afford: Many lenders prefer that mortgages account for no more than 28% of a borrower’s gross monthly income. However, you’ll need to account for all of your other monthly debts, including credit cards, student loans or car payment. Keep a lender’s maximum loan amount in mind, but also determine what you are comfortable spending each month.

- Check your credit: Your credit score may influence what loans you’re eligible for, so check your credit report. If you find any errors, dispute them as soon as possible.

- Get pre-approved: A pre-approval letter shows you the interest rate, loan amount and potential terms you’re likely to qualify for. Request pre-approval early so you have a better idea of your budget and can make an offer when you find the right house.

- Compare offers: After you’re pre-approved by a few lenders, compare your offer letters and find the best deal for you. Look at interest rates, terms and mortgage point costs.

- Look for a home: Browse homebuying sites, find a real estate agent, and start looking for the right home. Once you’ve found the one you want, make an offer and negotiate with the seller.

- Complete the mortgage application: After your offer is accepted, you will need to complete a mortgage application with your lender. You may need to submit additional financial documents. Submit these as soon as possible so you don’t delay closing.

- Wait for approval: Once your documents have been submitted, your application moves to underwriting. During this time, your lender verifies your financial documents and information to determine whether to extend the loan.

- Prepare for closing: You’ll then typically be scheduled for a closing date. Before then, you’ll need to arrange homeowners insurance and review your closing disclosures.

- Close: At closing, you’ll pay closing costs, make your down payment and sign transfer documents. Once you do, you’re officially a homeowner.

FAQ

What is the typical interest rate for a $600,000 mortgage?

Open

How does a 15-year vs. 30-year mortgage affect payments?

Open

Can I get a $600,000 mortgage with less than 20% down?

Open

How do I calculate my $600,000 mortgage payment?

Open