Credible takeaways

- A 3/1 adjustable-rate mortgage (ARM) is a type of mortgage that has a fixed interest rate for the first three years and a variable rate for the remainder of the loan term.

- The typical repayment term for a 3/1 ARM is 30 years, which means the rate will adjust once a year for 27 years.

- A 3/1 ARM initially offers a lower interest rate, but later payments can be unpredictable.

An adjustable-rate mortgage (ARM) is a type of mortgage where the interest rate can change at regular intervals following an initial fixed period. With a 3/1 ARM, the initial interest rate remains fixed for three years. Then, it can change in one-year intervals for the rest of the loan term.

By taking out a 3/1 ARM, your monthly payments might be lower for a few years. But if the rate increases, your monthly mortgage payments will also rise. A 3/1 ARM can be a good idea if you plan to refinance your home before the fixed period expires.

What is a 3/1 ARM loan?

An adjustable-rate mortgage is a type of home loan with an interest rate that can change over the life of the loan.

Here’s what the two numbers in an ARM mean:

- The first number: Indicates how long you’ll have a fixed rate

- The second number: Indicates how often the rate can reset per year following the fixed period

If you take out a 3/1 ARM, you’ll receive a fixed rate for the first three years of the loan. Then, based on several factors, the rate may increase or decrease once a year for the rest of your loan term.

Expert tip

“The housing market can be unpredictable, so make sure you know what to expect long term. If you have to delay your plans to move or refinance, make sure you’d be comfortable with the ongoing costs.” — Valerie Morris, Editor, Mortgages

ARMs generally become more popular when their interest rates are significantly lower than fixed-rate mortgages and home prices are on the rise. There’s not much of an advantage to choosing an adjustable rate when fixed interest rates are comparable, however, so most borrowers tend to stick with fixed-rate loans when rates are similar. In fact, the National Mortgage Database reported that only 3.9% of outstanding mortgages at the end of 2024 had an adjustable rate, down from the same period in 2023.

Learn More: What Is a Mortgage Rate and How Do They Work?

How a 3/1 ARM works

At the beginning of your mortgage, ARMs work just like fixed-rate loans. You take out a home loan with a fixed interest rate and make a monthly mortgage payment to your lender.

But three years into the mortgage, the lender might adjust your interest rate — along with your mortgage payment.

Here’s a closer look at how 3/1 ARMs work:

Changing rates

Lenders usually tie the ARM’s variable interest rate to one of three indexes:

- The maturity yield on 1-year Treasury bills

- The 11th District Cost of Funds index

- Secured Overnight Financing Rate (SOFR)

The LIBOR — once a popular index for mortgages — was phased out and replaced by Secured Overnight Financing Rate (SOFR) in June 2023.

Your lender will tell you which index your rate follows. The interest on your loan will be whatever the index rate is, plus a margin that the lender adds.

For example

If your margin is 2 percentage points and the SOFR is 4.15%, then your interest rate would be 6.15%.

The index rate can change, but the margin stays the same each time the rate resets. There are also limits — or caps — to how much the interest rate can increase.

Find Out: ARM vs. Fixed Mortgage: How to Choose Between Them

Interest rate caps

The interest rate on an adjustable-rate mortgage can rise or fall. Certain rules guide the rate movement. These are often expressed as a cap structure. One of the most common rate cap structures is the 2/2/5 cap structure.

Here’s what this means:

- Initial adjustment cap: The first number represents the maximum amount of percentage points that your interest rate can increase by in the first year after your initial fixed period ends. For a 3/1 ARM with a 2/2/5 cap structure, that means your rate can’t adjust to more than 2 percentage points higher than your initial rate in the fourth year of your loan.

- Subsequent adjustment cap: Your rate will adjust every year thereafter for the remainder of your loan. The cap for these adjustments is represented by the second number. With a 2/2/5 cap structure, your rate can only adjust a maximum of 2 percentage points.

- Lifetime rate cap: This limits how high the rate can rise over the life of the loan. In the case of a 2/2/5 cap structure, the third number shows that your interest rate cannot increase more than 5 percentage points over the life of the loan.

Loan terms

Every time your lender adjusts your interest rate, it also recalculates the mortgage payment so you pay off the loan by the end of your term. Adjustable-rate mortgages usually have 30-year loan terms.

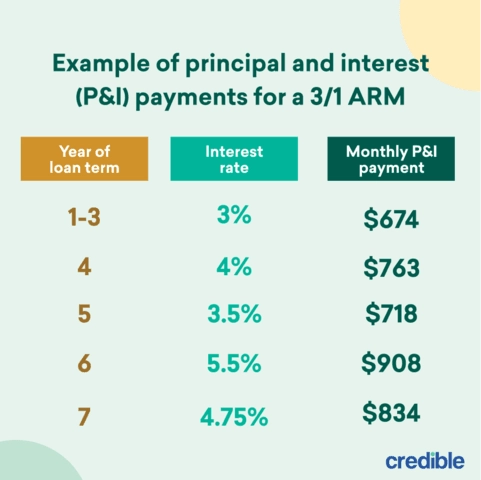

Let’s say you’re looking to buy a home worth $200,000 with a 20% down payment. Your lender offers you a 3/1 ARM with an initial rate of 3% and a cap structure of 2/2/5.

Take a look at how the interest rate might change over the first seven years under these terms and what it does to the principal and interest (P&I) payment:

On the other hand: If you took out a 30-year fixed-rate mortgage for the same home, your mortgage payments would be more predictable.

If your interest rate is set at 3.5%, then your monthly P&I payment will remain at $718 until you pay off the loan or refinance.

Pros and cons of a 3/1 ARM

A 3/1 adjustable-rate mortgage can provide low loan payments for three years, but the unpredictability beyond that point is your main enemy here. Consider these pros and cons before taking out a 3/1 ARM:

Pros

- Low initial payments: With a 3/1 ARM, your low mortgage payment is locked in for the first three years.

- Flexibility: You can decide to refinance your home loan once the fixed-rate period ends, or sell the home before the adjustable phase starts.

- Some built-in protection: ARMs come with rate and payment caps, which limit how high your interest rate and monthly payment can go.

- Your payments may decrease: If interest rates fall, then your monthly payment could drop, too.

Cons

- Your payments may increase: If interest rates rise, your monthly mortgage payment may go up. This could throw off your budget.

- Unpredictability: You might plan to sell your home or refinance your mortgage once the fixed-rate period ends. But if you’re unable to, and your rate increases, you might have trouble paying your mortgage.

- Prepayment penalty: Some ARMs come with a prepayment penalty, a fee the lender charges if you sell or refinance the home loan within a certain time frame. If you plan to sell or refinance, make sure your mortgage contract doesn’t include this penalty.

When to consider a 3/1 ARM

A 3/1 adjustable-rate mortgage could make sense if you:

- Don’t think you’ll stay in the home for the entire loan term.

- Plan to refinance the mortgage before the mortgage rate adjusts. However, you’ll need to consider whether rates will climb, if you’ll qualify for the best APR, and how much you’ll pay in closing costs.

To figure out if you’ll save money, compare 3/1 ARM interest rates with 30-year fixed rates. Ask the lender which index influences the ARM interest rates and whether the loan comes with rate caps.

Then, go over your budget and figure out if you can afford to pay the mortgage at its peak rate. If you can’t afford that payment, then an ARM may not be a good choice for you.

FAQ

How is a 3/1 ARM different from other types of ARMs?

Open

How does the interest rate change with a 3/1 ARM?

Open

How do I find a good ARM interest rate?

Open