The Federal Reserve Bank of New York reported earlier this month that household debt reached a record $18.04 trillion, increasing by $93 billion, in the fourth quarter of 2024. We’ll look at debt and delinquency rates across the different types of credit and why it matters.

Alert: Consumer confidence plummeted in February, according to the Conference Board’s monthly Consumer Confidence Index released Feb. 25. The Index dropped seven points, the biggest monthly decline since August 2021, with the Expectations Index dropping to 72.9, potentially indicative of a recession. According to the Index, the downturn resulted from the expected impact of tariffs, the rising cost of household staples, and stubborn inflation.

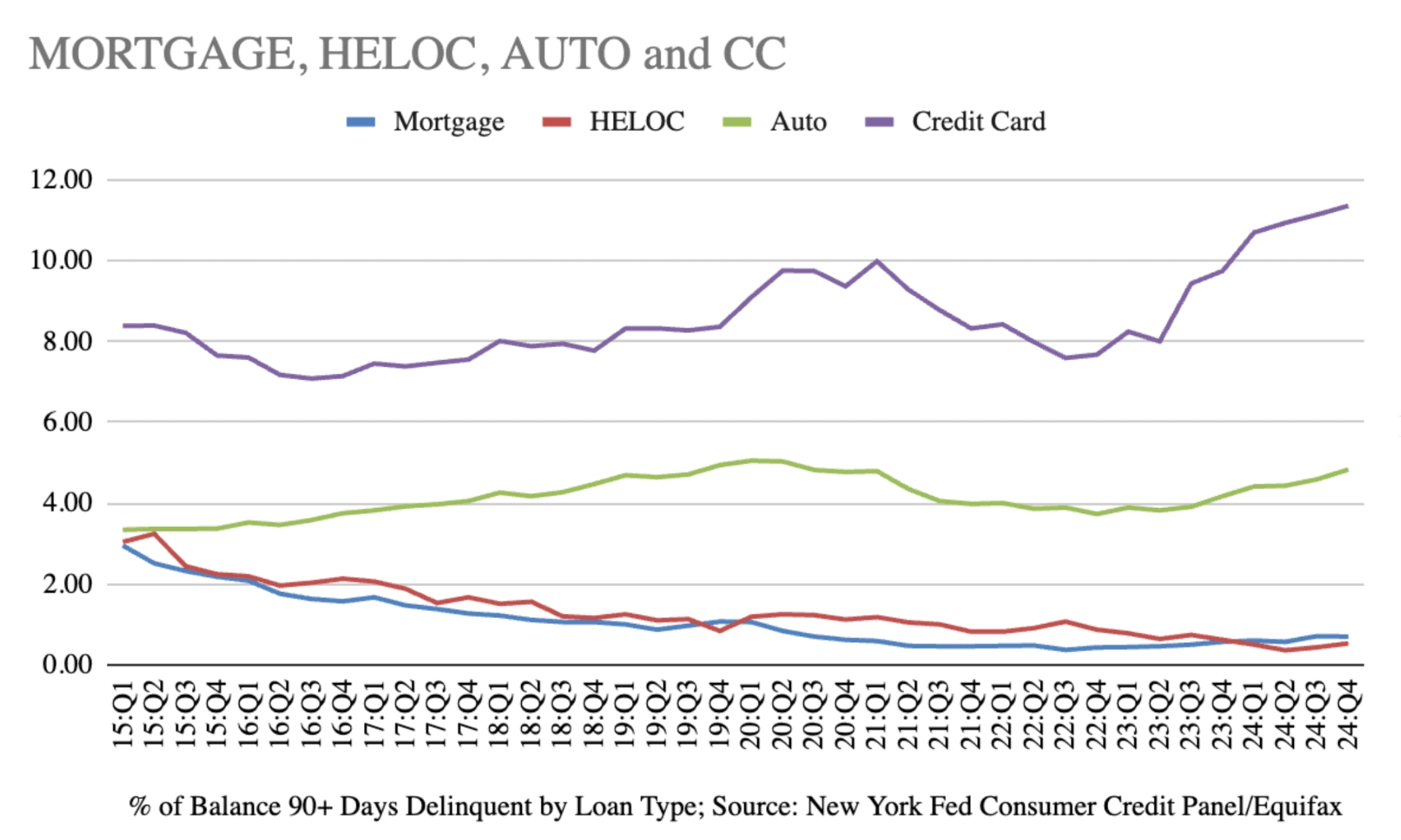

Household debt on the rise

Debt levels are increasing across the credit spectrum as more borrowers struggle to make minimum payments on their credit cards and auto loans.

- Credit card debt: Credit card balances increased by $45 billion from the previous quarter to a record $1.21 trillion at the end of December 2024, up 7.3% year-over-year. Delinquencies rose also, with more balances transitioning from current to delinquent status.

- Mortgage debt: Mortgage balances increased by $112 billion, reaching $12.44 trillion. However, delinquency rates for mortgages remain relatively low compared to other debt types, but have generally trended up since 2021.

- Auto loans: Auto loan balances rose to $1.61 trillion, with more borrowers struggling to make payments. Auto loan delinquencies have been creeping up, particularly among subprime borrowers.

- Student loans: Federal student loan payments resumed in late 2023 after a multi-year pause, contributing to a higher rate of missed payments in this category.

- Home equity lines of credit (HELOCs): HELOC balances also saw slight growth.

Tip

Delinquency occurs when a borrower misses a scheduled payment on a debt, such as a credit card, mortgage, or auto loan.

Delinquencies are trending up

The overall delinquency rate edged up to 3.6% of outstanding debt, a 0.1 percentage point increase from the previous quarter, with most of the increase attributable to auto loans and credit cards.

Accounts newly transitioning into delinquency (30 days or more late) ticked up for credit cards and mostly stayed steady for auto loans.

Serious delinquencies (accounts 90 or more days late) increased for both auto loans and credit card accounts — nearing and above decade-highs, respectively.

This suggests that more borrowers are struggling to keep up with payments, and those already struggling are not finding relief.

What is delinquency, and why does it matter?

Delinquency occurs when a borrower misses a scheduled payment on a debt, such as a credit card, mortgage, or auto loan. If delinquency continues, it can escalate into serious delinquency (90 days or more past due), which can have severe consequences, including:

- Damage to credit scores: Late payments negatively impact credit scores, making it harder to secure loans or favorable interest rates in the future.

- Penalty interest rates and fees: Missed payments often trigger penalty interest rates and late fees, making the debt even harder to pay off.

- Risk of default: If delinquency continues for too long, the lender may close the account, send the debt to collections, or pursue legal action.

Potential impacts of rising debt and delinquencies

As household debt continues to rise, keeping an eye on delinquency trends is crucial for understanding financial stability across the U.S. economy.

Economic impacts

While untenable on an individual level, when more consumers can't pay monthly debts, it can impact the larger economy as well. This could be in the form of less consumer spending and tighter lending standards, which we're already seeing. A 2024 Fed survey of consumer expectations and credit access indicated increased rejection rates for credit cards, mortgages, auto loans, credit card limit extension applications, and mortgage loan refinance applications — rejections for auto loans and mortgage refinances reached the highest level since the survey began in 2013.

Rising debt and delinquency rates can also be a sign that incomes aren't sufficient to keep up with inflation and the increasing costs of goods and services. Alternatively, they may also indicate increasing unemployment. But the latter isn't borne out by the current unemployment rate as reported by the Bureau of Labor Services.

Individual solutions

Individuals faced with high-interest debt, such as credit card debt, may be able to refinance it or consolidate multiple debts with a lower-rate loan, such as a personal loan.

According to the Fed's latest rate data, the difference between average APRs on credit cards and 24-month personal loans is substantial — credit card rates are over nine percentage points higher. Those who qualify to refinance credit card debt could potentially save hundreds or even thousands annually, while locking in a fixed interest rate and fixed monthly payments.

Personal loans are particularly advantageous if you don't have sufficient home equity to qualify for a home equity loan or would prefer not to tap it to pay unsecured debt.

Good to know

"The Federal Reserve cited the risk of rising inflation when they declined to cut interest rates in January, indicating that the cost of borrowing is unlikely to go down in the near future."

For more detailed information, access the full Quarterly Report on Household Debt and Credit here.