Credible takeaways

- Your credit score isn't a factor for federal student loans, though your credit history is considered for Direct PLUS Loans.

- The minimum credit score for private student loans varies by lender, but lenders generally look for a FICO score of at least 670.

- Adding a cosigner with excellent credit to your application can help you get approved for a private student loan at a lower interest rate.

In the 2025-26 academic year, the average published price for tuition and fees for full-time undergraduate students was $11,950 at public, in-state four-year schools, and $45,000 at private four-year schools, according to the College Board. This doesn't account for additional costs like books and room and board. With prices so high, student loans are a necessary tool for many college students.

The credit score you need for a student loan depends on the loan type and lender, and it can vary widely. Here's what you need to know about what credit score you need for student loans.

Current private student loan rates

What credit score do you need for federal student loans?

Most federal student loans — including Direct Subsidized and Unsubsidized Loans — don't require a credit check. That's why these loans make a good option for students who need help paying for school but don't yet have established credit histories.

But if you'd like to take out a Direct PLUS Loan, you must undergo a credit check. While you don't need a specific credit score to qualify for a PLUS Loan, you can't have an adverse credit history.

For the purposes of federal student loans, an adverse credit history means:

- You have a history of missed or late payments on at least one credit card or loan.

- You're 90 days or more delinquent on more than $2,085 of total debt.

- Your debt has been placed in collections or written off by the lender.

Additionally, if you've had any of the following on your credit report in the past five years, the Department of Education will view it as adverse credit history:

- Default determinations

- Debts discharged in bankruptcy

- Property foreclosures

- Property repossessions

- Tax liens

- Wage garnishment

- Federal student loan debt write-offs

You may still qualify for a federal PLUS loan with an adverse credit history. You’ll either have to apply with an endorser or submit documentation that the negative mark was caused by extenuating circumstances. You’ll also need to go through PLUS counseling.

Learn More: Direct PLUS Loans: A Guide for Parents and Graduate Students

What credit score do you need for private student loans?

You'll generally need a credit score of at least 670 to qualify for a private student loan, although some lenders don't disclose their minimum credit score requirements. However, the higher your score, the more likely you are to qualify for a lower interest rate.

If you have a poor credit score or limited credit history, you may be better off applying with a cosigner who has strong credit. This can increase your chances of approval and help you qualify for better loan terms.

How does your credit score affect your student loan interest rate?

Your credit score isn't a factor in your eligibility for federal student loans — everyone who takes out a federal loan in the same academic year receives the same rate. However, your credit score is a major factor in the credit score you receive for a private student loan.

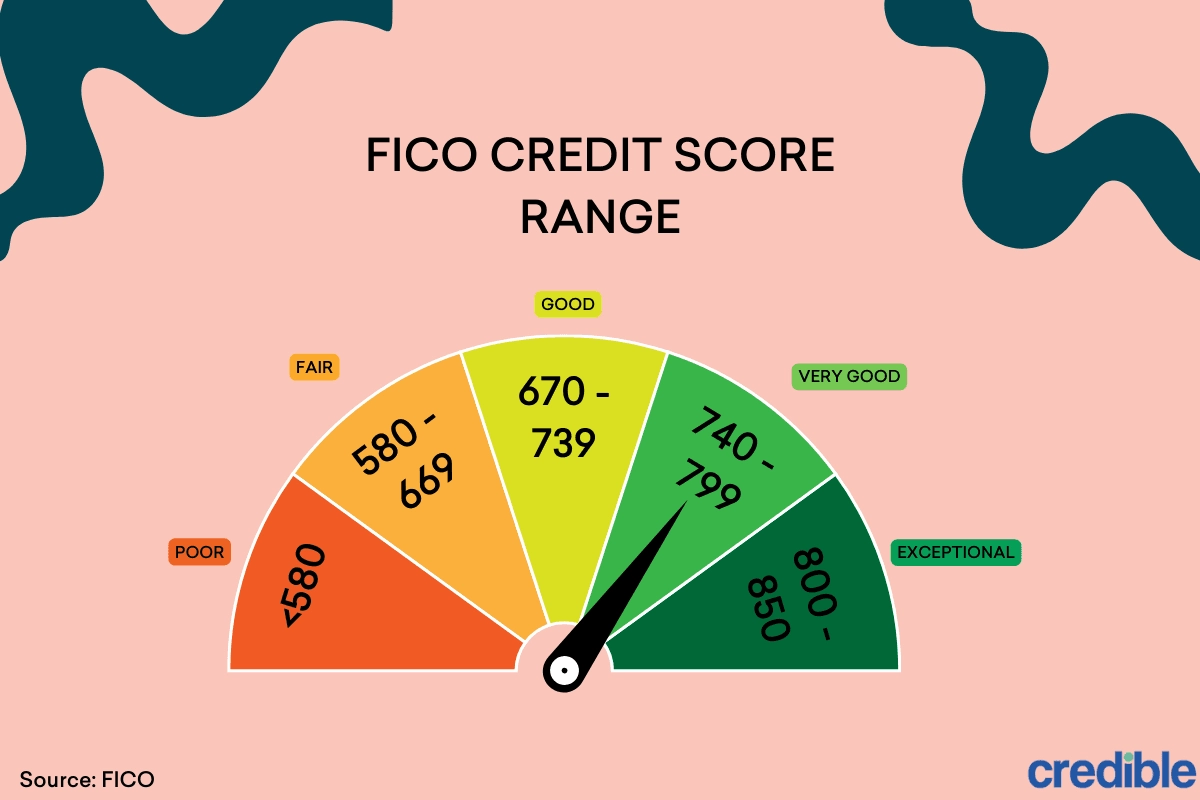

Private lenders can use various credit scoring models, but many consider your FICO credit score when reviewing your application. FICO scores range from 300 to 850, with the following categories:

The better your credit score, the better your odds of approval and the higher the rate you're likely to receive. While most lenders look for a minimum FICO score of 670, even those with “good” credit scores don't receive the highest rates. The best rates go to borrowers with exceptional credit. Meanwhile, those with “poor” credit scores receive the lowest rates, if they qualify for a loan at all.

The chart below shows average prequalified interest rates based on credit scores for borrowers who used the Credible marketplace to find a lender:

Student loan cosigner credit score minimum

Many students ask a parent to cosign their student loan. But if your parent doesn’t have good credit or isn’t comfortable cosigning, don’t worry — a cosigner can actually be anyone with good credit. For example, you could ask another relative or a trusted friend. Just remember that your cosigner will be on the hook for the loan if you can’t make your payments.

Since a cosigner shares responsibility for the loan, they need to show that they can manage the loan. This includes having good to excellent credit — usually a credit score of at least 670 or higher — as well as reliable income and a low debt-to-income ratio (DTI).

Keep in mind that individual lenders might also have their own requirements for student loan cosigners.

What to know about cosigner release

Cosigner release is a process that allows you to remove your cosigner from a loan. If you can prove to your lender that you can pay the loan on your own, your lender may remove your cosigner, and they'll no longer share responsibility for paying the loan.

You'll typically need to make a certain number of on-time payments and meet credit score and income requirements in order to qualify for cosigner release. However, it's important to note that not all private lenders offer this option.

The Credible student loan partner lenders in the table below offer student loans with the possibility of cosigner release.

Advertiser DisclosureThe rates that appear are from companies from which Credible receives compensation. This compensation does not impact how or where products appear within the table. The rates and information shown do not include all financial service providers or all of the displayed lenders' available services and product offerings.

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

$1,000 up to school-certified cost of attendance (aggregate $225,000 limit, $350,000 limit for certain discipline specific graduate loans)

Overview

Abe's private student loans are available to undergraduates, graduate students, and students enrolled in graduate certificate programs. Abe is unique in allowing you to borrow even if you're enrolled less than half-time.

Abe offers rate discounts and payment relief that other lenders don't, such as a reduction in your rate with autopay and for every six months of consecutive on-time principal and interest payments, up to a total of 0.50 percentage points. Borrowers can also extend their grace period up to an additional six months or up to nine months for Abe Law students. Plus, you can lengthen your repayment term by five years, which can be helpful if you need to lower your monthly payments or request a hardship forbearance for up to 12 months.

pros

- Offers 2% principal reduction after graduation

- Doesn’t charge late fees

- Can reduce interest rate by making on-time payments

- Possible repayment term and grace period extension

cons

- Doesn't allow parents to borrow on behalf of their child

- Student loan refinancing not available

Minimum income

$1 (must have positive income)

Loan terms

5, 7, 10, 15, or 20 years

Loan amounts

$1,000 up to school-certified cost of attendance (for undergrad loans; $350,000 for graduate loans)

Cosigner release

Available after making 12 consecutive on-time monthly principal and interest payments

Eligibility

Must be a U.S. citizen or permanent resident. Available to international students and DACA recipients attending a Title IV-eligible school in the U.S. who apply with a cosigner who is a U.S. citizen or permanent resident alien. Lender Disclosures

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Overview

While Ascent provides traditional student loans for undergraduate, graduate, and medical programs, it also stands out with some options that are uncommon among private student loan lenders. For example, its Outcomes-Based Loan, which doesn't require established credit or a cosigner, is available to juniors and seniors. When assessing your application, Ascent considers factors including your school, major, and GPA to determine if you're eligible.

Ascent also offers its Progressive Repayment plan to qualified borrowers. It allows you to begin with smaller payments at the start of the repayment term and then gradually pay more each month over time. If you borrow with a cosigner, they can be released after you make as few as 12 monthly payments. However, cosigners on loans for international students do not qualify.

pros

- Doesn’t charge application fees or origination fees

- Offers discounts of 0.50 to 1 percentage points when making automatic payments

- Can get a 1% cash-back reward after you graduate

- Grace periods from 9 to 36 months

cons

- May find lower interest rates with some competitors

- International students don’t have option to release cosigners

Loan terms

5, 7, 10, 12, 15, or 20 years

Loan amounts

$2,001 minimum up to your school’s annual cost of attendance; lifetime limits of $200,000 for undergrads and $400,000 for graduates

Eligibility

Must be a U.S. citizen or DACA student enrolled at least half time at an eligible institution. International students with a qualified cosigner may also qualify. Applicants who can’t meet financial, credit, or other requirements may qualify with a cosigner.

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

$1,000 up to 100% of the school-certified cost of attendance

Overview

Citizens Bank offers private student loans for undergraduate and graduate students, as well as parents. With its multiyear approval option, you can apply for a loan once, and as long as you qualify, you won't need to reapply each year. This means you can secure loans for future academic years without multiple hard credit checks.

Citizens borrowers can also take advantage of interest rate discounts. If you or your cosigner has an account with Citizens Bank, you can reduce your rate by 0.25 percentage points. Another 0.25 percentage points can be shaved off by enrolling in automatic payments, giving you the chance to lower your rate by up to 0.5 percentage points.

pros

- Multiyear approval lets you secure funding for future school years

- You can reduce your rate by 0.5 percentage points with autopay and loyalty discounts

- International students can apply with a qualified cosigner

- Cosigner release available after starting full principal and interest repayment

cons

- Fewer repayment terms to choose from than some other lenders

- Parents can’t defer payments while student is in school

- Must be enrolled at least half-time in a degree-granting program

Loan terms

5, 10, or 15 years for student loans; 5 or 10 years for parent loans

Loan amounts

Minimum $1,000, up to 100% of the school-certified cost of attendance

Cosigner release

After starting full principal and interest repayment

Eligibility

Must be a U.S. citizen or permanent resident enrolled at least half-time in a degree-granting program at an eligible institution. International students can apply with a cosigner who’s a U.S. citizen or permanent resident.

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

$1,000 up to 100% of the school-certified cost of attendance

Overview

College Ave offers student loans for almost every type of degree program, with a range of repayment options, including a unique 8-year repayment term. Additionally, you can get extended grace periods of as long as 36 months on graduate, dental, and medical student loans.

About 90% of undergraduates applying with a cosigner are approved for additional student loans. However, you must complete at least half of your repayment term before you can remove a cosigner for your loan. Some lenders allow cosigners to be released much sooner, after as few as 1 to 2 years of payments.

pros

- Rate discount of one-quarter of a percentage point for using autopay

- Does not charge origination or application fees

- Grace periods between 9 and 36 months for graduate, MBA, law, dental, and medical school loans

cons

- Parent borrowers are required to pay at least the interest while the student is in school

- Cosigners not eligible for release until at least half the repayment term of the loan is completed

Loan terms

5, 8, 10, or 15 years for most borrowers (law, dental, medical, and other health profession students have up to 20 years)

Loan amounts

$1,000 minimum up to your school’s annual cost of attendance; lifetime limits depend on your degree and credit profile

Cosigner release

Available after more than half of the scheduled repayment period has elapsed and other requirements are met

Eligibility

Must be a U.S. citizen or permanent resident at an eligible institution. International students with a Social Security number and a qualified cosigner may also qualify. Applicants who can’t meet financial, credit, or other requirements may qualify with a cosigner.

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

$1,000 up to school-certified cost of attendance (aggregate $225,000 limit)

Overview

Custom Choice is a student loan lender that offers loans ranging from $1,000 to $225,000 per year. Undergraduates, grad, and graduate certificate students can borrow up to a lifetime limit of $225,000.

You can get a 0.25% autopay discount, and up to a 0.25% on-time payment discount, plus a 2% principal reduction for graduating with at least a bachelor’s degree. You may apply with a cosigner if you can't qualify on your own, and you can release them after making 12 consecutive on-time principal and interest payments.

Custom Choice doesn't charge any fees whatsoever, even late fees. The lender also offers a forbearance program that lets you pause payments if you experience a financial hardship, an existing or persisting medical condition, a natural disaster, or suffer temporary unemployment.

pros

- You can reduce your rate by 0.5 percentage points with autopay and on-time payments

- Cosigner release available after 12 consecutive on-time monthly principal and interest payments

cons

- No mobile app for managing student loans

- Does not offer refinancing options for existing student loans

Minimum income

$1 (must have positive income)

Loan terms

5, 7, 10, 15, or 20 years

Loan amounts

$1,000 to $225,000 per year (lifetime limit of $225,000)

Cosigner release

After making 12 consecutive on-time principal and interest payments

Eligibility

Available to borrowers in all 50 states. The student must be a U.S. citizen or permanent resident alien, and must be the legal age of majority at the time of application or at least 17 years of age if applying with a cosigner who meets the age of majority requirements in the cosigner's state of residence. Eligible noncitizens, such as international students and DACA residents, can also qualify by applying with a cosigner who’s a U.S. citizen or permanent resident. Lender Disclosures

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

$1,001 up to 100% of school certified cost of attendance

Overview

INvested is an Indiana company that offers affordable student loans exclusively to state residents. Loans are available to Indiana students and parents who can meet income and credit requirements, or who have an eligible cosigner. Borrowers can borrow as little as $1,001 or as much as the school-certified cost of attendance minus other aid.

INvested provides detailed information on eligibility so borrowers can quickly determine whether to apply for a loan — however, there’s no option to prequalify with a soft credit check. Cosigner release is also available after just 12 on-time payments, considerably shorter than many other lenders.

pros

- Low minimum borrowing limits

- Autopay discount of 0.25 percentage points

- Short cosigner release requirements

- Transparent qualification requirements

cons

- No prequalification option to view your rates

- No loan options for international students

Loan amounts

$1,001 minimum, up to the school certified cost of attendance

Eligibility

Loans are available to Indiana residents only. Borrowers must have a FICO score of 670 or higher, a 30% maximum debt-to-income ratio or minimum monthly income of $3,333, continuous employment over two years, and no major collections or defaults in recent years. Borrowers who do not meet income or credit requirements can apply with a cosigner.

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

$1,500 up to school’s certified cost of attendance less aid

Overview

Massachusetts Educational Financing Authority (MEFA) offers student loans to borrowers with good credit. However, you won't be able to see your potential rate before applying.

The lender doesn't charge any fees and its rates are competitive, though MEFA only offers two repayment terms. You can add a cosigner to your loan if you're unable to qualify, but only one repayment plan allows you to release your cosigner.

pros

- Doesn’t charge any fees

- Low maximum rate compared with some lenders

- Can borrow up to the school-certified cost of attendance

cons

- No discounts for borrowers

- Limited repayment terms

- No prequalification available

Loan amounts

$1,500 minimum up to school-certified cost of attendance

Eligibility

Must be a U.S. citizen or permanent resident, enrolled at least half time at a degree-granting, nonprofit institution, and must maintain satisfactory academic progress. Must have no history of default on an education loan and no history of bankruptcy or foreclosure in the past 60 months. Applicants who can’t meet the minimum credit and income requirements may apply with a cosigner.

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Overview

Nelnet Bank (Member FDIC) provides private student loans at competitive rates for undergraduate, graduate, and health professional degrees. You'll need a FICO credit score in the mid to high 600s to qualify. Borrowers with bad credit can apply with a cosigner, which may help them qualify and could reduce their interest rate.

Cosigners on Nelnet student loans can be released after 24 consecutive on-time payments (see disclaimer). You can also get a 0.25% interest rate reduction when you sign up for automatic payments (see disclaimer). There are no loan origination or application fees, but Nelnet does charge fees for late payments of insufficient funds.

pros

- Rates are competitive for borrowers or cosigners with strong credit

- Rate discount of 0.25 percentage points for autopay

- Cosigners can be released after 24 on-time payments

- Offers deferment and payment assistance programs

cons

- Charges fees for late payment and insufficient funds

- Doesn’t guarantee deferment and forbearance options

Loan terms

5,10,15* (IO, Deferred, Immediate)

Loan amounts

$1,000 to $125,000 for undergraduate, $1,000 to $175,000 for graduate, $1,000 to $500,000 for graduate health professions

Eligibility

All states and US Territories

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

$1,000 up to 100% of school-certified cost of attendance

Overview

Sallie Mae offers the Smart Option Student Loan for undergraduate students and a suite of loans for graduate students. You can borrow up to your school-certified cost of attendance and apply just once annually to get the funds you need for the entire academic year. Plus, applying for a Smart Option Student Loan with a cosigner may help you get a better rate.

Through Sallie Mae, you can find a variety of loans designed for specific needs, including loans for MBA programs, law school, medical school, and health profession programs.

pros

- Can borrow up to school-certified cost of attendance

- No prepayment or origination fees

- Loans available to noncitizens with an eligible cosigner

- Cosigner release after 12 on-time payments

cons

- No parent loan options

- Does not offer student loan refinancing

- Loan terms not disclosed until after you apply

Loan terms

10 to 15 years for the Smart Option Student Loan; 15 years for law school, MBA, and graduate school loans; 20 years for medical school loans

Loan amounts

$1,000 up to school-certified cost of attendance. Student must be listed as the borrower, and a parent may cosign.

Cosigner release

After you graduate, make 12 one-time principal and interest payments, and meet certain credit requirements

Eligibility

Must be a U.S. citizen or permanent resident enrolled in an eligible program. Noncitizens residing and attending school in the U.S. may qualify by applying with a creditworthy cosigner, who must be a U.S. citizen or permanent resident, and providing an unexpired government-issued photo ID.

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Overview

SoFi offers fixed- and variable-rate student loans to help undergraduate, graduate, and professional students and parents of students finance their education. These loans can cover up to the total cost of attendance, with a minimum loan of $1,000. Students must be enrolled at least half-time in a degree-seeking or graduate-certificate program at an eligible school and a U.S. citizen, permanent resident, or non-permanent resident alien.

SoFi has multiple repayment plans, allowing students to pick terms that best fit their financial situations, with cosigner release after 12 months of consecutive on-time payments. Borrowers have the option to reduce rates by 0.25% when enrolling in automatic payments. They can also qualify for a 0.125% interest rate discount on subsequent loans with SoFi's Continuing Scholar Discount. Plus, a $250 cash bonus with a 3.0 GPA or higher for full-year loans or $100 cash back for single-semester loans.

Lender Disclosures

pros

- Top customer service ratings

- Valuable member benefits

- No fees

- Cosigner release after 12 months of on-time payments

cons

- No disclosed credit or income requirements

- Shorter repayment terms than some lenders

Loan amounts

$1,000 minimum up to your school’s annual cost of attendance

Eligibility

Must be a U.S. citizen or DACA student enrolled at least half-time at an eligible institution. International students with a qualified cosigner may also qualify. Applicants who can’t meet financial, credit, or other requirements may be eligible with a cosigner.

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Loan Amounts

$1,000 up to school-certified cost of attendance (aggregate $225,000 limit, $350,000 limit for certain discipline specific graduate loans)

Overview

Abe's private student loans are available to undergraduates, graduate students, and students enrolled in graduate certificate programs. Abe is unique in allowing you to borrow even if you're enrolled less than half-time.

Abe offers rate discounts and payment relief that other lenders don't, such as a reduction in your rate with autopay and for every six months of consecutive on-time principal and interest payments, up to a total of 0.50 percentage points. Borrowers can also extend their grace period up to an additional six months or up to nine months for Abe Law students. Plus, you can lengthen your repayment term by five years, which can be helpful if you need to lower your monthly payments or request a hardship forbearance for up to 12 months.

pros

- Offers 2% principal reduction after graduation

- Doesn’t charge late fees

- Can reduce interest rate by making on-time payments

- Possible repayment term and grace period extension

cons

- Doesn't allow parents to borrow on behalf of their child

- Student loan refinancing not available

Minimum income

$1 (must have positive income)

Loan terms

5, 7, 10, 15, or 20 years

Loan amounts

$1,000 up to school-certified cost of attendance (for undergrad loans; $350,000 for graduate loans)

Cosigner release

Available after making 12 consecutive on-time monthly principal and interest payments

Eligibility

Must be a U.S. citizen or permanent resident. Available to international students and DACA recipients attending a Title IV-eligible school in the U.S. who apply with a cosigner who is a U.S. citizen or permanent resident alien. Lender Disclosures

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Overview

While Ascent provides traditional student loans for undergraduate, graduate, and medical programs, it also stands out with some options that are uncommon among private student loan lenders. For example, its Outcomes-Based Loan, which doesn't require established credit or a cosigner, is available to juniors and seniors. When assessing your application, Ascent considers factors including your school, major, and GPA to determine if you're eligible.

Ascent also offers its Progressive Repayment plan to qualified borrowers. It allows you to begin with smaller payments at the start of the repayment term and then gradually pay more each month over time. If you borrow with a cosigner, they can be released after you make as few as 12 monthly payments. However, cosigners on loans for international students do not qualify.

pros

- Doesn’t charge application fees or origination fees

- Offers discounts of 0.50 to 1 percentage points when making automatic payments

- Can get a 1% cash-back reward after you graduate

- Grace periods from 9 to 36 months

cons

- May find lower interest rates with some competitors

- International students don’t have option to release cosigners

Loan terms

5, 7, 10, 12, 15, or 20 years

Loan amounts

$2,001 minimum up to your school’s annual cost of attendance; lifetime limits of $200,000 for undergrads and $400,000 for graduates

Eligibility

Must be a U.S. citizen or DACA student enrolled at least half time at an eligible institution. International students with a qualified cosigner may also qualify. Applicants who can’t meet financial, credit, or other requirements may qualify with a cosigner.

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Loan Amounts

$1,000 up to 100% of the school-certified cost of attendance

Overview

Citizens Bank offers private student loans for undergraduate and graduate students, as well as parents. With its multiyear approval option, you can apply for a loan once, and as long as you qualify, you won't need to reapply each year. This means you can secure loans for future academic years without multiple hard credit checks.

Citizens borrowers can also take advantage of interest rate discounts. If you or your cosigner has an account with Citizens Bank, you can reduce your rate by 0.25 percentage points. Another 0.25 percentage points can be shaved off by enrolling in automatic payments, giving you the chance to lower your rate by up to 0.5 percentage points.

pros

- Multiyear approval lets you secure funding for future school years

- You can reduce your rate by 0.5 percentage points with autopay and loyalty discounts

- International students can apply with a qualified cosigner

- Cosigner release available after starting full principal and interest repayment

cons

- Fewer repayment terms to choose from than some other lenders

- Parents can’t defer payments while student is in school

- Must be enrolled at least half-time in a degree-granting program

Loan terms

5, 10, or 15 years for student loans; 5 or 10 years for parent loans

Loan amounts

Minimum $1,000, up to 100% of the school-certified cost of attendance

Cosigner release

After starting full principal and interest repayment

Eligibility

Must be a U.S. citizen or permanent resident enrolled at least half-time in a degree-granting program at an eligible institution. International students can apply with a cosigner who’s a U.S. citizen or permanent resident.

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Loan Amounts

$1,000 up to 100% of the school-certified cost of attendance

Overview

College Ave offers student loans for almost every type of degree program, with a range of repayment options, including a unique 8-year repayment term. Additionally, you can get extended grace periods of as long as 36 months on graduate, dental, and medical student loans.

About 90% of undergraduates applying with a cosigner are approved for additional student loans. However, you must complete at least half of your repayment term before you can remove a cosigner for your loan. Some lenders allow cosigners to be released much sooner, after as few as 1 to 2 years of payments.

pros

- Rate discount of one-quarter of a percentage point for using autopay

- Does not charge origination or application fees

- Grace periods between 9 and 36 months for graduate, MBA, law, dental, and medical school loans

cons

- Parent borrowers are required to pay at least the interest while the student is in school

- Cosigners not eligible for release until at least half the repayment term of the loan is completed

Loan terms

5, 8, 10, or 15 years for most borrowers (law, dental, medical, and other health profession students have up to 20 years)

Loan amounts

$1,000 minimum up to your school’s annual cost of attendance; lifetime limits depend on your degree and credit profile

Cosigner release

Available after more than half of the scheduled repayment period has elapsed and other requirements are met

Eligibility

Must be a U.S. citizen or permanent resident at an eligible institution. International students with a Social Security number and a qualified cosigner may also qualify. Applicants who can’t meet financial, credit, or other requirements may qualify with a cosigner.

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Loan Amounts

$1,000 up to school-certified cost of attendance (aggregate $225,000 limit)

Overview

Custom Choice is a student loan lender that offers loans ranging from $1,000 to $225,000 per year. Undergraduates, grad, and graduate certificate students can borrow up to a lifetime limit of $225,000.

You can get a 0.25% autopay discount, and up to a 0.25% on-time payment discount, plus a 2% principal reduction for graduating with at least a bachelor’s degree. You may apply with a cosigner if you can't qualify on your own, and you can release them after making 12 consecutive on-time principal and interest payments.

Custom Choice doesn't charge any fees whatsoever, even late fees. The lender also offers a forbearance program that lets you pause payments if you experience a financial hardship, an existing or persisting medical condition, a natural disaster, or suffer temporary unemployment.

pros

- You can reduce your rate by 0.5 percentage points with autopay and on-time payments

- Cosigner release available after 12 consecutive on-time monthly principal and interest payments

cons

- No mobile app for managing student loans

- Does not offer refinancing options for existing student loans

Minimum income

$1 (must have positive income)

Loan terms

5, 7, 10, 15, or 20 years

Loan amounts

$1,000 to $225,000 per year (lifetime limit of $225,000)

Cosigner release

After making 12 consecutive on-time principal and interest payments

Eligibility

Available to borrowers in all 50 states. The student must be a U.S. citizen or permanent resident alien, and must be the legal age of majority at the time of application or at least 17 years of age if applying with a cosigner who meets the age of majority requirements in the cosigner's state of residence. Eligible noncitizens, such as international students and DACA residents, can also qualify by applying with a cosigner who’s a U.S. citizen or permanent resident. Lender Disclosures

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Loan Amounts

$1,001 up to 100% of school certified cost of attendance

Overview

INvested is an Indiana company that offers affordable student loans exclusively to state residents. Loans are available to Indiana students and parents who can meet income and credit requirements, or who have an eligible cosigner. Borrowers can borrow as little as $1,001 or as much as the school-certified cost of attendance minus other aid.

INvested provides detailed information on eligibility so borrowers can quickly determine whether to apply for a loan — however, there’s no option to prequalify with a soft credit check. Cosigner release is also available after just 12 on-time payments, considerably shorter than many other lenders.

pros

- Low minimum borrowing limits

- Autopay discount of 0.25 percentage points

- Short cosigner release requirements

- Transparent qualification requirements

cons

- No prequalification option to view your rates

- No loan options for international students

Loan amounts

$1,001 minimum, up to the school certified cost of attendance

Eligibility

Loans are available to Indiana residents only. Borrowers must have a FICO score of 670 or higher, a 30% maximum debt-to-income ratio or minimum monthly income of $3,333, continuous employment over two years, and no major collections or defaults in recent years. Borrowers who do not meet income or credit requirements can apply with a cosigner.

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Loan Amounts

$1,500 up to school’s certified cost of attendance less aid

Overview

Massachusetts Educational Financing Authority (MEFA) offers student loans to borrowers with good credit. However, you won't be able to see your potential rate before applying.

The lender doesn't charge any fees and its rates are competitive, though MEFA only offers two repayment terms. You can add a cosigner to your loan if you're unable to qualify, but only one repayment plan allows you to release your cosigner.

pros

- Doesn’t charge any fees

- Low maximum rate compared with some lenders

- Can borrow up to the school-certified cost of attendance

cons

- No discounts for borrowers

- Limited repayment terms

- No prequalification available

Loan amounts

$1,500 minimum up to school-certified cost of attendance

Eligibility

Must be a U.S. citizen or permanent resident, enrolled at least half time at a degree-granting, nonprofit institution, and must maintain satisfactory academic progress. Must have no history of default on an education loan and no history of bankruptcy or foreclosure in the past 60 months. Applicants who can’t meet the minimum credit and income requirements may apply with a cosigner.

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Overview

Nelnet Bank (Member FDIC) provides private student loans at competitive rates for undergraduate, graduate, and health professional degrees. You'll need a FICO credit score in the mid to high 600s to qualify. Borrowers with bad credit can apply with a cosigner, which may help them qualify and could reduce their interest rate.

Cosigners on Nelnet student loans can be released after 24 consecutive on-time payments (see disclaimer). You can also get a 0.25% interest rate reduction when you sign up for automatic payments (see disclaimer). There are no loan origination or application fees, but Nelnet does charge fees for late payments of insufficient funds.

pros

- Rates are competitive for borrowers or cosigners with strong credit

- Rate discount of 0.25 percentage points for autopay

- Cosigners can be released after 24 on-time payments

- Offers deferment and payment assistance programs

cons

- Charges fees for late payment and insufficient funds

- Doesn’t guarantee deferment and forbearance options

Loan terms

5,10,15* (IO, Deferred, Immediate)

Loan amounts

$1,000 to $125,000 for undergraduate, $1,000 to $175,000 for graduate, $1,000 to $500,000 for graduate health professions

Eligibility

All states and US Territories

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Loan Amounts

$1,000 up to 100% of school-certified cost of attendance

Overview

Sallie Mae offers the Smart Option Student Loan for undergraduate students and a suite of loans for graduate students. You can borrow up to your school-certified cost of attendance and apply just once annually to get the funds you need for the entire academic year. Plus, applying for a Smart Option Student Loan with a cosigner may help you get a better rate.

Through Sallie Mae, you can find a variety of loans designed for specific needs, including loans for MBA programs, law school, medical school, and health profession programs.

pros

- Can borrow up to school-certified cost of attendance

- No prepayment or origination fees

- Loans available to noncitizens with an eligible cosigner

- Cosigner release after 12 on-time payments

cons

- No parent loan options

- Does not offer student loan refinancing

- Loan terms not disclosed until after you apply

Loan terms

10 to 15 years for the Smart Option Student Loan; 15 years for law school, MBA, and graduate school loans; 20 years for medical school loans

Loan amounts

$1,000 up to school-certified cost of attendance. Student must be listed as the borrower, and a parent may cosign.

Cosigner release

After you graduate, make 12 one-time principal and interest payments, and meet certain credit requirements

Eligibility

Must be a U.S. citizen or permanent resident enrolled in an eligible program. Noncitizens residing and attending school in the U.S. may qualify by applying with a creditworthy cosigner, who must be a U.S. citizen or permanent resident, and providing an unexpired government-issued photo ID.

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Overview

SoFi offers fixed- and variable-rate student loans to help undergraduate, graduate, and professional students and parents of students finance their education. These loans can cover up to the total cost of attendance, with a minimum loan of $1,000. Students must be enrolled at least half-time in a degree-seeking or graduate-certificate program at an eligible school and a U.S. citizen, permanent resident, or non-permanent resident alien.

SoFi has multiple repayment plans, allowing students to pick terms that best fit their financial situations, with cosigner release after 12 months of consecutive on-time payments. Borrowers have the option to reduce rates by 0.25% when enrolling in automatic payments. They can also qualify for a 0.125% interest rate discount on subsequent loans with SoFi's Continuing Scholar Discount. Plus, a $250 cash bonus with a 3.0 GPA or higher for full-year loans or $100 cash back for single-semester loans.

Lender Disclosures

pros

- Top customer service ratings

- Valuable member benefits

- No fees

- Cosigner release after 12 months of on-time payments

cons

- No disclosed credit or income requirements

- Shorter repayment terms than some lenders

Loan amounts

$1,000 minimum up to your school’s annual cost of attendance

Eligibility

Must be a U.S. citizen or DACA student enrolled at least half-time at an eligible institution. International students with a qualified cosigner may also qualify. Applicants who can’t meet financial, credit, or other requirements may be eligible with a cosigner.

How to get a student loan with bad credit

If you have bad credit, you may have other options besides federal student loans and cosigned private loans.

Some private lenders offer student loans for bad credit. But these loans typically come with higher interest rates than good-credit loans, which could drive up the overall cost of your loan.

Expert insight: “I recommend checking your credit report for free at AnnualCreditReport.com before prequalifying or applying with lenders. It's a good way to see where your credit stands and whether there's anything you can improve. If you spot any errors, you can also dispute them with the credit bureaus to help boost your score.”

— Renee Fleck, Student Loans Editor, Credible

How to check your credit score

You’re entitled to a free copy of your credit report from each of the three credit-reporting bureaus — Equifax, Experian, and TransUnion — once per year.

You can use Credible's free credit monitoring tool to request these reports and review your credit history easily. If you find any errors in your credit reports, dispute them with the appropriate credit bureaus to potentially boost your score.

However, your credit reports generally don’t include your credit score. You can check your credit score for free through your bank, credit card issuer, or a free online service. You can also request your score directly from the credit bureaus.

Tip

It’s a good idea to monitor your credit score regularly. This way, you can keep an eye on any changes and look out for errors or fraud.

How to raise your credit score

To get the most competitive rates or increase your chances of being approved for a student loan without a cosigner, here are some tips on how to raise your credit score:

- Get a secured credit card and keep up with monthly payments.

- Monitor your credit history and dispute any mistakes.

- Ask to raise your credit limit if you have an existing credit card.

- Become an authorized user on someone else’s credit card.

- Pay down existing loans on time.

FAQ

What is the minimum credit score for a student loan?

Open

Federal student loans don't have minimum credit score requirements. With private student loans, most lenders want you to have a credit score of around 670 or higher. Keep in mind that the minimum credit score can vary depending on the lender. If you don't have great credit, you'll probably need a cosigner to get approved.

What credit score do I need for a federal student loan?

Open

Your credit score isn't a factor for federal student loans. However, your credit history is a factor for Direct PLUS Loans. You can't qualify for a PLUS loan with an adverse credit history, which includes a recent history of default determinations, property foreclosures, or tax liens, among other serious credit issues. If you add an endorser to your application or you can prove you had extenuating circumstances, you may still be able to take out a PLUS loan.

What credit score do I need for a private student loan?

Open

Each private lender has its own credit score criteria. However, you'll generally need a FICO score of 670 or higher to qualify for a private student loan. The best rates are reserved for those with the highest credit scores.

Do I need a cosigner for a private student loan?

Open

While a cosigner isn't required for private student loans, you likely won't qualify without one if you have no credit, poor credit, or little to no credit history. Adding a cosigner with excellent credit and a steady income to your application can improve your approval odds and help you qualify for a lower interest rate.

How can I improve my credit score?

Open

You can boost your credit score by making payments on your debts on time, disputing any inaccuracies in your credit report with the appropriate bureau, becoming an authorized user on a loved one's credit card, or getting a secured credit card and keeping up with payments.

Sarah Li-Cain contributed to the reporting for this article.

Meet the expert:

Emily Guy Birken

Emily Guy Birken is an authority on student loans and personal finance. Her work has been featured by MSN Money and MarketWatch.